Welcome back.

Let’s join us

Reset password

Is There A Financial Crisis Around The Corner?

Heading 2

Paragraph

Heading 3

A rich text element can be used with static or dynamic content. For static content, just drop it into any page and begin editing. For dynamic content, add a rich text field to any collection and then connect a rich text element to that field in the settings panel. Voila!

Heading 4

Headings, paragraphs, blockquotes, figures, images, and figure captions can all be styled after a class is added to the rich text element using the "When inside of" nested selector system.

Heading 5

Following a strong performance in 2023 with the S&P rising by 26.29%, recovering from an 18.11% setback in 2022, the market is approaching this year with a sense of caution. The Federal Reserve's announcement of interest rate reductions led to the market hitting new historic highs, a milestone unseen since December 2021.

However, this goal didn't offer investors the expected reassurance about the state of the economy. Instead, market participants noticed that this surge was primarily driven by monetary policy rather than company performance.

Lower interest rates can create an illusion that promotes speculation rather than reflecting the reality of a robust and healthy economy. As a result, smart money sees potential volatility for 2024.

Real Economy and Mixed Market Sentiment

The market is currently at historic highs, yet it's challenging to find people who assert that the economy is in good shape. This prevailing sentiment among the public is also echoed by many companies and analysts.

For instance, according to a Resume Builder report, 4 out of every 10 companies expect to lay off employees in 2024, and half say anticipation of a recession is a reason for making people redundant. We must also consider the effects of inflation on consumers' purchasing power. In an election year, these factors become crucial.

Key sectors in the economy are showing early signs of vulnerability due to the impact of stringent financial conditions. The Institute of Supply Management reported a contraction in manufacturing activity for the 14th consecutive month in December.

Regarding the financial market, opinions are mixed. Goldman Sachs expects the S&P 500 to have an acceptable return of 8% this year, based on current equity valuations and higher GDP growth. Other big players like Bank of America, also forecast a decent 2024, with a 5.3% increase.

However, JPMorgan's view diverges from much of Wall Street. The bank's chief global equity strategist, Dubravko Lakos-Bujas, expressed concerns about global growth deceleration, shrinking household savings, and heightened geopolitical risks, especially with upcoming elections in the US, that could contribute to policy volatility.

According to the largest bank in the United States, the S&P 500 is expected to close the year at 4200 points, reflecting an 11% decline.

These mixed sentiments are indicative of various concerns, but probably, the most significant risk at the moment is the disconnection of current market prices from the actual state of the economy and the expectations of the Federal Reserve.

The Fed's Handling of Interest Rates

Despite core inflation hovering around 4% annually, the Federal Reserve is confident in its ability to keep inflation near the 2% mark, and after a recent board meeting in December, members suggested that there would be three rate cuts throughout 2024.

The market swiftly responded to this news. The Federal Reserve's pivot towards increased liquidity propelled the market to historic highs, with speculative assets like Bitcoin experiencing substantial gains. The euphoria is such that current bond prices indicate the market is anticipating five rate cuts, more than what the FED disclosed.

However, the viability of all FED commitments and current price levels hinges on a genuine reduction in inflation. The crucial question we need to ponder is: what if the reduction in inflation stalls and stays above 2%?

Higher-than-expected inflation and failure to meet market expectations would significantly erode valuations. There are several reasons to believe that this could happen. To illustrate, the initial data for 2024 regarding inflation was negative, as headline Consumer Price Inflation turned out to be hotter than expected in December.

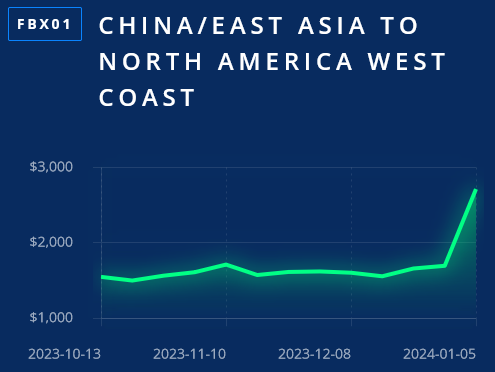

Moreover, in just the first days of January, escalating acts of piracy in the Middle East led to approximately a 60% surge in freight costs for transporting a container from China to the United States and a 250% increase in China-Europe transportation costs.

In essence, the transportation costs of goods from key trading partners to the United States has significantly increased, adding pressure to producers, distributors, and eventually, consumers.

Interestingly, market expectations are notably more optimistic than both the Federal Reserve's predictions and the actual reality. As a result, even slight deviations in inflation or expectations can lead to significant volatility.

Real Estate

Real Estate is another key sector of the economy, and as we've explored in recent articles, it also looks volatile. Record costs of mortgages, the erosion of purchasing power since 2019, and pessimistic expectations about the future of the market are some of the problems this market is facing.

The Fed is now navigating a delicate balance between addressing inflationary pressures and managing systemic risks to the American economy.

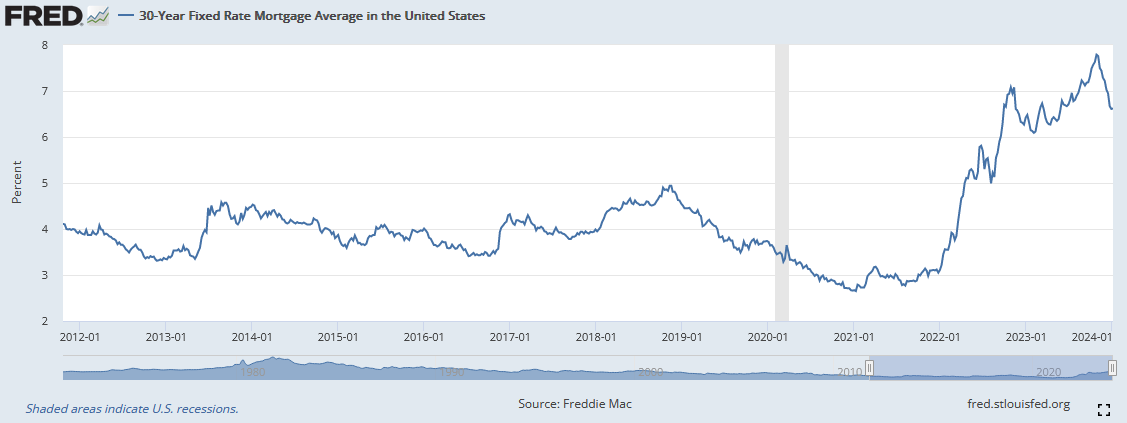

Driven by the benchmark rates, 30-year mortgage rates rose to the highest levels in two decades, reaching values close to 7.5%.

High rates are the only thing keeping inflation in check - but with many companies (and homeowners) hopelessly overleveraged following over a decade of easy-money policy, sustaining high interest rates could prove just as devastating.

Affordability and Expectations

The purchasing power of families, a primary driver in the real estate market, has been decreasing since 2019. According to official data from the US Census Bureau, the real median income of households declined by 5.3% in recent years. However, simultaneously, housing prices reached new highs in 2023.

It seems challenging for this disparity to persist. We should wonder if real estate developers have quietly acknowledged this issue, which might be the reason housing starts have been decreasing continuously since 2022, as we can see in the chart below.

Finally, market expectations for real estate are mostly negative. According to Zillow, home prices in 34 out of the 50 largest cities in the United States show signs of decline.

If this holds true, it could potentially set off an unprecedented chain reaction scenario, with real incomes falling for a record number of years, and, similar to the 2008 financial crisis, families grappling with properties whose value is lower than their nominal debt.

The primary victims of this crash would be individuals looking forward to retirement, as they would witness their lifelong savings wiped out by a 33 trillion dollar credit bubble in the United States that, at some point, must deflate.

Conclusion

With all of these factors at play, the smart money is ignoring bullish reassurances and entering 2024 with caution. Despite claims to the contrary, we're not out of the woods yet, and the aftershocks of the pandemic continue to be felt. With the Fed playing a dangerous game, trying to lower inflation by maintaining high rates, 2024 could be the year that the other shoe finally drops.

Whether or not this happens, adding more diversification to your portfolio is a smart move this year. With Farmfolio's farmland assets, you can easily own international farmland without breaking the bank. Get in touch with our staff to learn more.

Gain insider access to Farmfolio's network.

Receive weekly insights and updates directly from Farmfolio.